The 'Exits' are Coming: Africa's Opening Act

Let the show begin!

👋 Hi there, Juan Gabriel here, and this is where I write about the ideas, companies and people redefining the future for the next billion internet users. Make sure to stay up to date by clicking this button to subscribe 👇🏻.

👋 Welcome again! Today, is the second part in my series The ‘Exits’ are Coming covering the massive entrepreneur / investor outcomes in emerging markets. If you missed my piece on Latin America with KASZEK’s Hernán Kazah, view it here. I’ll cover other regions in future pieces until we become 👇👇

👀 Recent Exits are Just a ‘Tease’

You may already know that Africa is the fastest growing continent in the world. But, in the midst of the pandemic of the century, you might have missed the fact that Africa is STILL the fastest growing region in the world. 7 out of 10 of the fastest-growing countries are African.

But 2020 was also beyond demonstrating the resilience of growth—but not necessarily health systems—in Africa. 2020 was the best year for multi-million dollar acquisitions and exits in the region. Several headline grabbing acquisitions were announced across the African tech ecosystem including WorldRemit’s $500 million purchase of Sendwave—a digital remittance service operating in Africa and Asia.

Notable Acquisitions of African startups in 2020

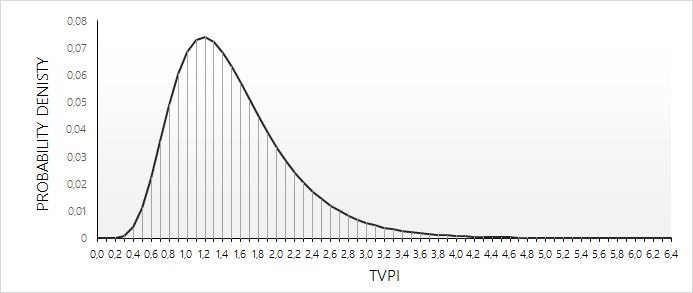

Combined, these three exits represent nearly $1 billion in exit value. What’s more they portray very promising Total Value to Paid in Capital (TVPI) transaction multiples —value realized/unrealized over total paid in capital—for the investors and entrepreneurs behind these companies. Take the example of Paystack (YC W16) a Nigeria-based payment processing platform where according to Pitchbook, investors —including its eventual buyer Stripe—had cumulatively invested $12 million and reaped a 16x multiple on this transaction. More simply, if you as an investor had cumulatively put in $1 million into Paystack, the value of the shares you owned after the purchase would hover around $16 million. Note: There are other things that would influence the actual value of the equity you own (e.g. dilution in certain rounds, transaction fees, and much, much more.) but because I don’t have visibility to the details of each deal, I’m keeping it simple. The takeaway is this: these are healthy multiples that validate product-market fit for VC-backed investments in Africa. Just consider, the relevant multiples for DPO and Sendwave are even higher: 19x and 34x, respectively.

Now, these ‘back of the envelope’ TVPI multiples are not perfect gauges of returns:

TVPIs are typically calculated for an entire fund, not on a transaction basis. Other transactions in the portfolio can drop the entire fund’s TVPI as most portfolio companies fail.

Actual returns will vary significantly by investor, stage and liquidation preferences. It is possible that some investors may earn 60-70x returns while others a more ‘humble’ 10x on this transaction depending on what each investor paid for equity.

TVPI does not take into consideration discount rates (the opportunity cost of investing this money elsewhere to earn a return).

Again, one thing is clear: these are the kind of returns that can validate venture investment and make VC economics work.

Source: Guillem

As shown above using public data from one of the largest Limited Partners (LPs) in US Venture Capital —the California Public Employees Retirement System (CalPERS)— most funds won’t yield a significant return on capital ( typically at least 3X). Frank Rotman, an investor at QED partners and legend in the fintech community lays it out for us:

Though these 2020 exits likely didn’t yield 100X returns for all investors, it sets the tone for what’s to come. Recent exits in the African tech ecosystem are the ‘opening act’ in VC-backed exits in the region. Open the curtains, let the show begin! 🎭

🚨 Africa is the fastest-growing VC market

Let me say it again, Africa is the fastest-growing VC market in the world. Africa’s rise is not just because of favorable demographic dynamics, it is the results of the budding ecosystem transforming lives for millions. It is also attitude, it is leadership, it is capital and it is globalization.

The number of VC-backed equity rounds in Africa has been rising since the ecosystem really started gaining global attention in 2015. Partech Partners, a Paris-based VC firm with excellent research has shown that “The global interest for the African tech ecosystem remains strong even in the context of the global crisis driven by the pandemic”. The numbers back it up.

359 deals may sound like rookie numbers compared to the +10,000 VC deals in the US but keep in mind that we are still in the beginning of the ‘hockey stick’ growth of VC activity in Africa. The CAGR of deal counts between 2015-202 0 is 46% per year, growing by almost half every single year.

Let’s dive deeper into the data. The total value of VC investments in Africa is also up from $277 million in 2015 to a recent peak of $2bn in 2019. Despite, a Covid-induced drop-off in 2020 ($1.4bn), this is good news.

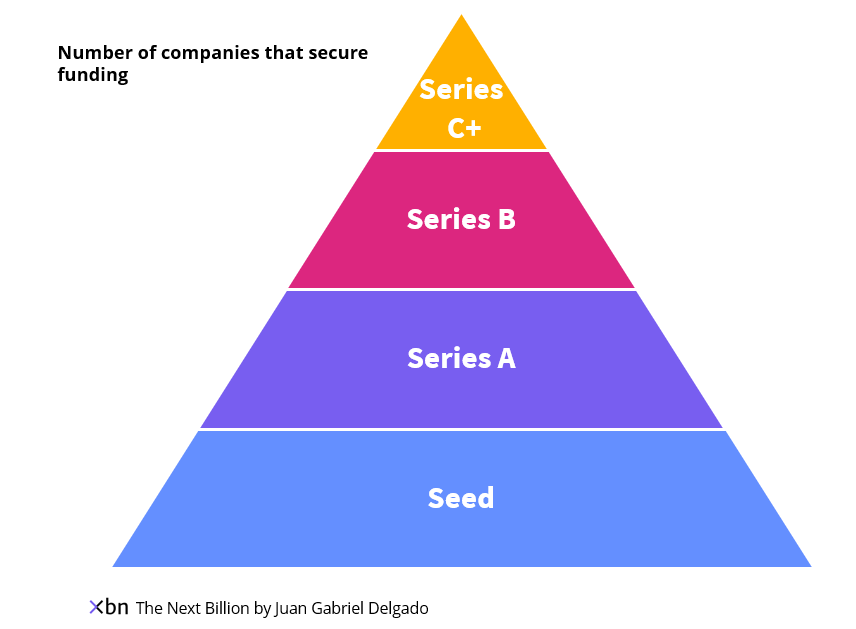

Let me explain. Very few companies make it to later stage funding rounds and even fewer reach a successful M&A Exit or IPO. CB Insights calls it a ‘funnel’ and has run some great analyses showing that only ~3% of US companies make it to the 6th round (~Series E).

Do me a favor, invert this ‘funnel’ and make it into a pyramid with a strong base and only a small tip. This might seem like semantics, but ecosystems are built on numerous early stage companies that experiment with different products and business models. This analogy matters. A ‘funnel’ implies that what matters is increasing conversion between stages. That’s great, but that’s not VC. VC is about massive and outlier returns at the top of the pyramid, a select number of companies that are truly “groundbreaking” (and fund-making, a single company paying back the whole fund). Failing is part of that process. So, a VC ecosystem requires a really ‘fat’ base of the pyramid to yield enough high quality companies at the top of the pyramid (below a fantastic PPT graphic for you 😂). If only 3% of companies make it to late-stage funding in the US where capital is ample, and infrastructure is in place, then its reasonable to think that the ratio would be lower (perhaps 1-2%) in Africa or Latin America. That requires a really, really large base of the pyramid in Africa.

Fortunately, that’s just what’s been happening in the African ecosystem: there’s been massive growth in deal count for Seed and Series A investments, a much faster clip than growth / late stage investments.

This is the sign of a maturing ecosystem. In the past, VC investors in Africa were just picking up high-quality companies with a proven traction and revenue, and giving them the capital to grow. In 2015, the ratio of Seed & Series A rounds to Series B & Growth rounds was perhaps 2:1 (just eyeballing here from the chart above). Now, in 2020 let’s say its more like 9:1 (again, just eyeballing here). The implication is clear: Africa is building a healthy pipeline of companies with transformative potential for the region’s economy and the next billion internet users.

🚨 Decades of Work

So, how did we get here? I think the African ecosystem has progressed across three distinct stages tolerating risk and market returns. I’ll be very brief and give you the gist of each.

1️⃣ Official Aid - the original non-capitalist

Official Development Aid (ODA) was the primary form of investment in Africa for decades. Soon after a wave of independence movements swept through Africa in the 1950s and 1960s, rich world countries and former colonial powers started providing ODA to African countries. Often, ODA was aligned with cold-war aims and the domestic interests of donor countries, which often tied aid flows conditional to purchases from donor country companies. I’m not here to detail the shortcomings of aid (plenty of people can do it better), but I do want to highlight how ODA was the original non-capitalist in Africa.

Source: Brookings

Aid flows have grown over time: reaching $40bn in 2016, up from $5bn in 1960 (numbers are likely much higher now as a result of Covid-19). During much of this time, ODA was main or even sole source of investment in Africa. Beyond extractives, private companies were mostly absent and national African governments had little capital to invest (still the case today). ODA has played a role building some of the very basic infrastructure that helped propel Africa to the next phase because ODAs were grants (the money was rarely expected back).

2️⃣ Impact Investors - Where no private actor would go

Over the past 10-20 years, the introduction of the Millennium Development Goals and their successors, the Sustainable Development Goals, have let to an acceleration of impact investing in Africa. Impact investors, motivated not exclusively by profit, started stepping in to fund companies and nonprofits that no private actors would fund, but which were beyond the purview or resources of ODA.

This was necessary to reach the third stage. Why? Because impact investors can pursue lower than market returns. The thinking of many Impact Investors is best exemplified by the “Returns Continuum” co-developed by my Stanford Professor Matt Bannick and his peers at the Omidyar Network.

The returns continuum evaluates three types of impact: Market Impact (how the firm shapes the market and creates new opportunities across the ecosystem), Firm Impact (directly experienced by customers), and Financial Return (how much capital would be returned to investors). While ODA invested in category C (Grants) where little monetary returns were expected but large impact was expected, Impact Investors could pursue Category B (Subcommercial) projects that have absolute positive returns, even if these were below market returns. Already, this opened up many opportunities to smartly allocated capital to do good. When you are targeting the ‘bottom billion’ and the poorest in a given country, it is likely you’ll need to index on lower absolute returns (you could invest that money in the US or Europe for market returns).

3️⃣ VC - From Venture to Frontier

Over the past five years, I think we’ve transitioned to a third stage where traditional venture firms (African and foreign) now actively operate in the African VC ecosystem. VC firms will target most of the Category A investments in the Returns Continuum above: market and not-market validated returns (basically “is this a tried and tested business model?”). They need to target these types of investments to make their economics work: VC in Africa is not Venture Philanthropy, its a genuine realization in the potential of massive companies and monetary returns are to be made. In fact, several Impact Investors I’ve spoken with now compete with traditional VC firms in Africa, and sometimes they lose out. That’s neither good nor bad, I think everyone has a role to play and many Impact Investors have knowledge and expertise that complements traditional VC investors.

Overall, this is a sign of a more complex system. Just take a look at this diagram on the African ecosystem from The Generalist’s Mario Gabriele:

We’ve got incubators and hubs: they cultivate the base of the pyramid. Media networks: they provide visibility and coverage to aspiring companies. Early Funds (including RallyCap Ventures to which I belong) that scout for promising talent and ideas. Growth funds, that give companies with traction the resources they need to become regional. Corporate VCs and Big Enterprise: they are investing in cutting edge tech that may disrupt their existing business models. Prominent companies: they provide brand names and motivation for talent and entrepreneurs. Finally, we’ve started to see major exits: they are what will validate these investments, and will mint millionaires that will become angel investors in the next generation of African companies.

Closing Thoughts

This is starting to get long, but TLDR: I’m very bullish on the African tech ecosystem.

The sheer numbers that surround this continent make it prominent to the world, but what excites me is the talent working to tackle Africa’s wicked problems. For all the progress that’s been going on, we are still at the early stages: less than a handful of African VC-backed tech companies have IPOd, instead, promising companies are snatched up by other larger (non-African) startups and corporates. I relish to see the day in the coming years where African tech companies go public in US or European exchanges to a global audience of investors (and perhaps a pan-African exchange in the longer-term). Heck, I’d even welcome a well-formed SPAC!

Further Reading

Smart and smart(er) than me!

Further Africa - Scaling Africa’s tech ventures to exit this decade

The Generalist - Tech in Africa

The Subtext - The Chicken or the Exit?

Alex Lazarow & Allen Taylor - The Promise of SPACs for Emerging Market

Techcrunch - Why SPACs aren’t targeting Africa

The Flip - Tech exits and the likelihood of an international listing

Thanks for reading 🙌 Feedback? Please. Building something for the next billion? Please reach out: on Twitter or LinkedIn. If you haven’t yet, please subscribe and share!

Let me know your thoughts on this piece!